Read time: 5 minutes

Encouraging trends in plan design

| 2013 | 2023 | |

| Plans with automatic enrollment | 34% | 59% |

| Automatic enrollment plans with 4%+ default | 35% | 60% |

| Average employer match value | 4.1% | 4.6% |

| Immediate eligibility | 61% | 74% |

| Participants offered target-date funds | 90% | 99% |

| Participants offered advice | 52% | 77% |

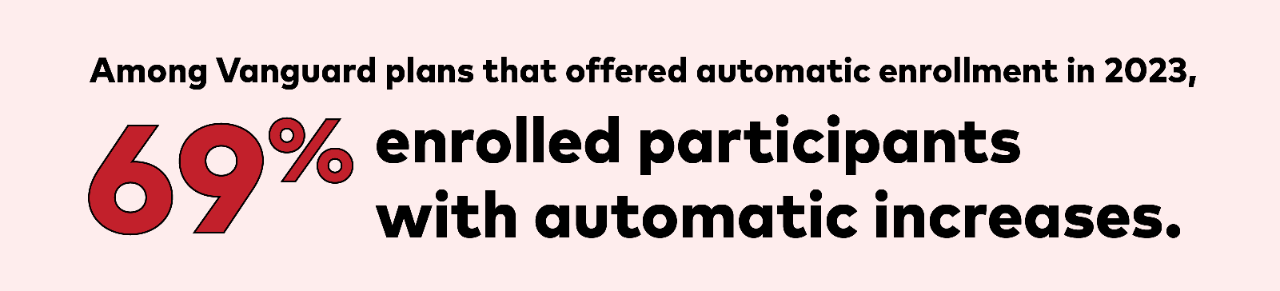

Automatic increases: The unsung hero

Automatic annual deferral rate increases are a powerful feature that can help improve participants’ chances for retirement success. Previous Vanguard research found that participants enrolled in a plan with automatic enrollment and automatic annual increases save, on average, 20% to 30% more after three years than participants in an automatic enrollment plan that doesn’t automatically enroll participants with annual increases.2 When the increase coincides with an annual pay raise, employees may not notice much difference in their take-home pay.

Figure 3 shows that among automatic enrollment plans, those most likely to enroll employees with automatic annual increases have employee default deferral rates of 3% and 4%. Plans with lower (1% to 2%) and higher defaults (5%, 6%, or more) are less likely to use automatic increases.

Plans that enroll employees at higher default deferral rates without automatic annual increases can also cause participants to anchor at lower saving rates, typically in line with the employer match value. In 2023, the average employer match value was 4.6%, and the maximum employee deferral rate to receive the full value of the match was typically 4% to 6%.

To reach a total saving rate of 12% to 15%, many participants need to save above the maximum match level unless their plan offers extraordinarily generous employer contributions. For plans defaulting at higher rates, including an annual increase probably won’t raise the cost of employer contributions if the plans are already defaulting participants at the maximum employer match rate.

The power of inertia

1Vanguard, How America Saves 2024.

2Vanguard, How Americans Can Save More for Retirement, 2023, p. 5.

Related items

Note:

- All investing is subject to risk, including the possible loss of the money you invest.