Senior Advice Strategist, Vanguard Workplace Solutions

Mr. Wolf is a senior advice strategist in Vanguard Participant Advice & Wellness. His focus is consulting with plan sponsors and consultants on Vanguard's advice and guidance offers for retirement plans. Most recently, Mr. Wolf served as head of Investment Services in Vanguard Financial Advisor Services™, leading Vanguard Advisor Portfolio Analytics and Consulting, Vanguard ETF® strategic model portfolios, and a team of national speakers responsible for sharing Vanguard thought leadership. Previously, Mr. Wolf led a team of senior financial advisors providing discretionary advice to Vanguard's highest-net-worth individual investors and their families. Earlier in his career, he was an investment analyst in Vanguard Portfolio Review Department, a relationship manager to nonprofit clients in Vanguard Institutional Asset Management, and a retirement education specialist in Vanguard Participant Education. Evan earned a B.A. from the University of Virginia and an M.B.A. from the Wharton School of the University of Pennsylvania. He is a CFP® professional.

Over the years, I’ve had countless conversations with plan sponsors and consultants about adding or changing a managed account1 program for their plans. I’ve seen every flavor of committee structure and every kind of decision-making process.

Some themes have emerged that I thought you might be interested in hearing about (thus the “peeking into your neighbors’ advice 'windows’” headline).

Let’s start with a straightforward but powerful fact: Adding or changing advice providers is a fiduciary decision. Fortunately, I rarely come across plan sponsors who take the decision lightly. There is broad recognition that the appropriate committee with fiduciary responsibility should be voting to adopt a new advice program. But the paths to get there often look different. I can plot these differences across three dimensions (don’t worry, there will be no actual plotting or statistical analysis in this blog):

- The “stretched thin” factor of the HR team.

- The involvement (if any) of a consultant.

- The mandate and meeting frequency of the committee.

Let’s explore each of them.

How thinly stretched is the HR team?

I have found that the plan sponsors who are most engaged in meaningful managed account discussions have the most focused jobs. (Too obvious? Stay with me. It gets more interesting.) When an HR contact is responsible for other duties like benefits or compensation, they have less bandwidth to go around. This is especially true when there are other big corporate activities underway like mergers, acquisitions, or systems migrations. When a contact’s role is more focused on workplace retirement plans (interestingly, these roles aren’t always correlated to the size of the organization), I have seen greater willingness and ability to understand what they have now, what their managed account options are, and what best meets the needs of their organization. Engagement from HR is critical to a thorough process, and I’ll expand on this further in the committee section below.

When an organization has finance or treasury experts involved in evaluating participant advice programs, it’s a way to share the work and have programs viewed through multiple lenses that take into consideration participant experience, fees, and methodology. Some of the most effective processes include HR and finance teams working closely together, leveraging a consultant along the way.

Speaking of consultants . . . is one involved?

Nearly every plan sponsor I’ve worked with has a relationship with a consultant, but rarely do two clients interact with consultants in the same way. I’ve seen tightly integrated, “full service” relationships; narrow engagements focused on fund lineup construction and oversight; and project-based relationships such as RFPs and 401(k) plan design changes. I think highly of myself, but not so highly that I feel it’s my place to opine on which arrangement is better. However, I often see the benefits of a plan sponsor soliciting (and documenting!) a consultant’s input on the pros, cons, and considerations for advice programs.

Each consulting firm has its own approach to evaluating managed account services. Some issue formal ratings and reports, others document and disseminate general information about leading offers, and some consider advice needs on a client-by-client basis. Certainly, there are benefits to working with a consultant who takes advice evaluation and oversight seriously, but there is no one right answer. Unlike funds, which are well suited to straightforward ratings, advice offers have many nuances. These nuances, which include participant experience, financial planning features, and methodology, may vary in relevance and importance from one plan sponsor to the next.

What’s the decision-making committee all about?

Congratulations if you’ve made it this far in the process! The final step is a committee with fiduciary responsibility. I’ve seen these committee structures vary from one organization to another. On one end of the spectrum are “401(k) committees” that really dig into a topic and might spend up to an hour vetting and voting on a managed account program. On the other end are “benefits committees” with broader mandates. Most committees only meet a few times a year, so getting time on their agendas can be challenging. In those cases, one of two things usually happens:

- The discussion stagnates because there are too many competing priorities.

- The HR team (often in partnership with a consultant) assumes more of the responsibility to vet the advice options, enabling the committee to do a more high-level review and vote on the HR team’s recommendation.

One last observation that may or may not resonate with you: There is sometimes uncertainty about which committee has responsibility for a decision. Is it the 401(k)/benefits committee or the investment committee? Or a combination? Participant advice has elements of plan design and investments within it, so the confusion is understandable. If you’re not sure, it might be worth confirming. You never know when you might want to review your existing or prospective advice providers!

What can an effective process look like?

Have I belabored the point enough about how evaluation of managed account programs can vary? I’ve seen plan sponsors make decisions in minutes, and I’ve worked with others who took years to vet a program. In my experience, here’s an effective process:

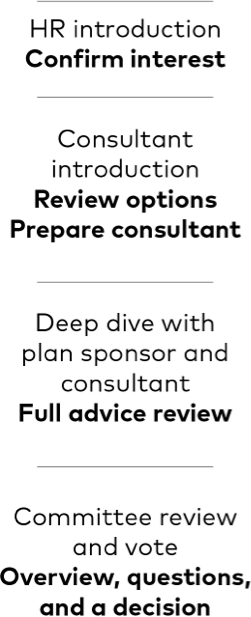

- HR introduction: 10 to 15 minute overview to confirm interest in spending more time on advice.

- Consultant introduction: 30 to 60 minute review of the options to ensure the consultant is prepared to assist the plan sponsor.

- Deep dive with the plan sponsor and consultant: 60- to 90 minutes for a full advice review.

- Committee review and vote: 30 to 45 minutes for an overview, questions, and a decision.

This approach incorporates the key stakeholders, building momentum and support before involving time-crunched committees.

Does the process take time? Yes.

But is it worth it? Also, yes! Advice isn’t the right fit for every participant, but for those who want it,2 it’s a critical piece of the financial well-being puzzle. In fact, Vanguard recently published some research3 using hypothetical case studies that show that the value of advice can range from 83 to 285 basis points annually (recognizing that the value for any participant could be above or below that).

In the coming months, I’ll write about how to monitor participant advice programs, how Vanguard’s advice methodology navigates volatile markets, how advice personalization can benefit employees, and how to move smoothly from one advice program to another.

In the meantime, if you have questions about the evaluation of our employee advice/managed account services in general, feel free to reach out to us.

Comments?

Ideas for future blog posts?

1 I promise to go easy on the footnotes, but you’ll need a few along the way. I use “advice” and “managed accounts” interchangeably, but I do recognize they can have different connotations. “Advice” sometimes is used to describe one-time, nondiscretionary support, while “managed accounts” often refers to ongoing, discretionary management. Vanguard uses “advice” to describe the full range of services.

2 Advice needs vary, but to give you a sense: per How America Saves 2022, 10% of participants with access to managed accounts chose to enroll.

3 Weber, Stephen M., Paulo Costa, Bryan Hassett, Sachin Padmawar, and Georgina Yarwood. The value of personalized advice. Vanguard, 2022.

More from the author

The right advice options for your plan

Employee advice

Notes:

- Past performance is not a guarantee of future returns.

- Advice is provided by Vanguard Advisers, Inc. (VAI), a federally registered investment advisor. Eligibility restrictions may apply. VAI cannot guarantee a profit or prevent a loss.

- Certified Financial Planner Board of Standards Inc. owns the certification marks CFP®, CERTIFIED FINANCIAL PLANNER™, in the U.S., which it awards to individuals who successfully complete the CFP Board's initial and ongoing certification requirements.