Read time: 7 min

To measure the impact of advice on an individual investor’s well-being, Vanguard’s new paper The Value of Personalized Advice introduces the Vanguard Financial Advice Model (VFAM) for quantifying the value of specific financial planning recommendations in the context of an overall plan.

VFAM allows us to quantify advice’s impact on a specific investor’s financial plan relative to their current strategy and demonstrates its principles using four hypothetical case studies: a high-income earner on his first job, a millennial couple invested primarily in a target-date fund, a couple preparing for retirement, and a retired couple with a sizeable nest egg.

The paper demonstrates how the most valuable advice interventions vary greatly and comprehensively between clients, based on their individual characteristics.

“Although we normally consider investment value quantitatively, we have focused on only qualitative measures to assess the financial and emotional value of advisor recommendations,” says Joel Dickson, head of Vanguard Enterprise Advice Methodology. “Being able to develop quantitative values for important financial planning objectives—such as maintaining reasonable spending patterns or mitigating small risks of disastrous outcomes for one’s plan—allows for a better comparison with investment values and a more complete view of opportunities and their impact on individual clients’ outcomes.”

Being able to develop quantitative values for important financial planning objectives...allows for a better comparison with investment values and a more complete view of opportunities and their impact on individual clients’ outcomes.

Joel Dickson, Ph.D.

Head of Vanguard Enterprise Advice Methodology

Vanguard views financial advice as an ongoing process focused on helping investors reach their goals, not simply an initial financial plan or portfolio allocation. Advice can provide value in many ways, whether delivered by human advisors or digital platforms.

Vanguard believes that the more personal an advice plan is, the more value it can deliver, at least before fees are considered. The discovery process to understand an investor’s aspirations for their life and financial future is critical for crafting a tailored and personal financial plan and delivering value.

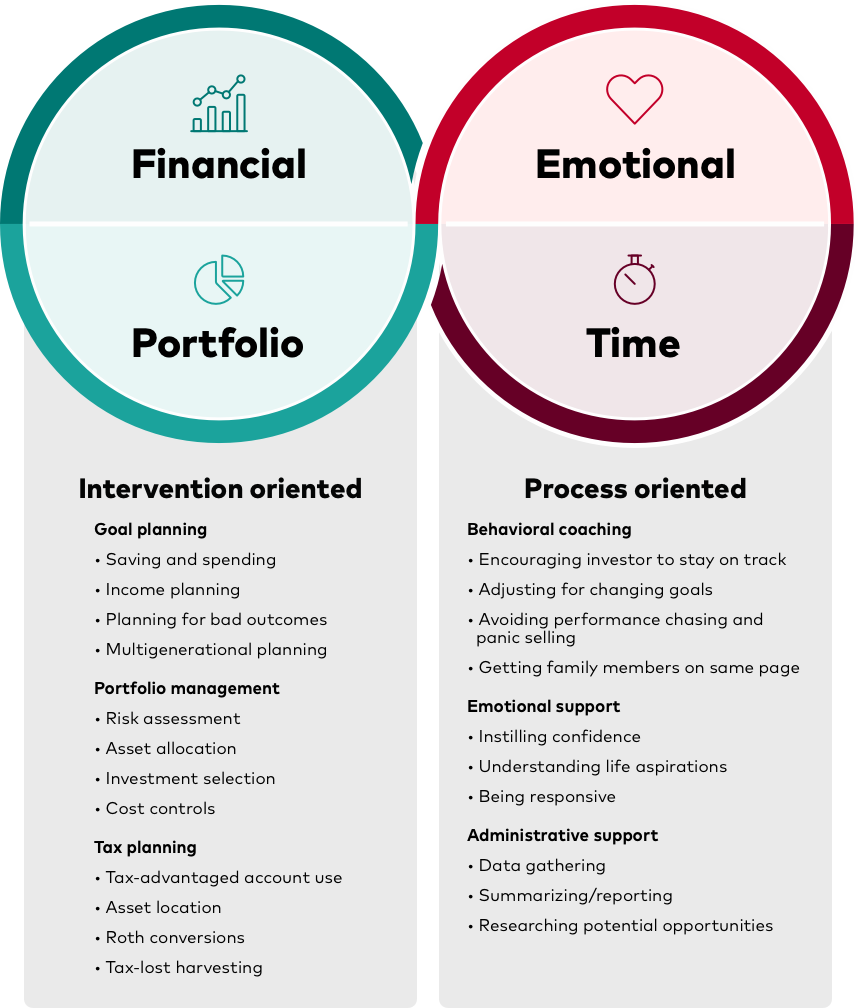

With this paper, Vanguard expands its traditional rubric for examining the value of advice (financial, portfolio, and emotional) to include time value because human advisors and digital advice platforms can perform tasks that individual investors might not have the time, willingness, or ability to perform on their own. Figure 1 shows how specific types of advice interventions and activities map to this value framework.

Figure 1. Sources of advice value

As demonstrated in the paper, VFAM establishes a baseline understanding of the investor’s current strategy and its range of potential outcomes. It then models advice interventions appropriate to the investor’s goals and needs, as well as the range of potential outcomes from those interventions. Finally, VFAM estimates how much additional wealth or extra annual return the investor would need to achieve (using their current approach) to match the estimated outcomes of the advised alternative.

“VFAM develops personalized recommendations based on unique client circumstances and assesses how much those recommendations would improve a client’s current approach or situation,” Dickson says. “By taking into account taxes, advice fees, uncertain market and inflation scenarios, and variable life expectancy outcomes, VFAM allows us to quantify the value of a specific investor’s financial plan relative to the current strategy.”

Figure 2 outlines these VFAM elements, including its use of the Vanguard Capital Markets Model® (VCMM) return simulations. Vanguard considers utility as a measure of the life satisfaction that wealth can provide. At lower wealth levels, an increase of a certain amount of wealth may have much greater utility than the same increase at higher wealth levels.

Figure 2. Elements of the Vanguard Financial Advice Model

VFAM concentrates on the impact of advice personalization at the individual investor level. This can be useful for helping identify and prioritize the specific interventions that are most valuable for each investor. It also measures the impact of multistrategy effects—when advice interventions work together to provide superior outcomes (for example, putting bonds in tax-advantaged accounts). In addition, the VFAM explicitly values and weights potential investment outcomes appropriately and accounts for the variability of life expectancy outcomes (versus a specific age).

Quantifying the value of the total financial plan and not just the portfolio can give clients a more accurate picture of where they stand relative to their long-term goals. Says Dickson, “Taking these steps and sticking with this holistic approach drives results beyond investment returns and increases the chances that clients will successfully reach their financial goals. This is the essence of advice-keeping clients on track to achieve them!”

More information

For more information on how Vanguard helps institutional clients’ employees navigate financial complexity, see:

Notes:

- IMPORTANT: The projections and other information generated by the Vanguard Capital Markets Model regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees of future results. VCMM results will vary with each use and over time.

- The VCMM projections are based on a statistical analysis of historical data. Future returns may behave differently from the historical patterns captured in the VCMM. More important, the VCMM may be underestimating extreme negative scenarios unobserved in the historical period on which the model estimation is based.

- The Vanguard Capital Markets Model® is a proprietary financial simulation tool developed and maintained by Vanguard’s primary investment research and advice teams. The model forecasts distributions of future returns for a wide array of broad asset classes. Those asset classes include U.S. and international equity markets, several maturities of the U.S. Treasury and corporate fixed income markets, international fixed income markets, U.S. money markets, commodities, and certain alternative investment strategies. The theoretical and empirical foundation for the Vanguard Capital Markets Model is that the returns of various asset classes reflect the compensation investors require for bearing different types of systematic risk (beta). At the core of the model are estimates of the dynamic statistical relationship between risk factors and asset returns, obtained from statistical analysis based on available monthly financial and economic data from as early as 1960. Using a system of estimated equations, the model then applies a Monte Carlo simulation method to project the estimated interrelationships among risk factors and asset classes as well as uncertainty and randomness over time. The model generates a large set of simulated outcomes for each asset class over several time horizons. Forecasts are obtained by computing measures of central tendency in these simulations. Results produced by the tool will vary with each use and over time.

- All investing is subject to risk, including the possible loss of the money you invest.

- Advice from Vanguard services are provided by Vanguard Advisers, Inc., a federally registered investment advisor, or by Vanguard National Trust Company, a federally chartered, limited-purpose trust company.