Read time: 5 minutes

Roth 401(k) overview

• Roth contributions are made on an after-tax basis, allowing participants to avoid taxes on their withdrawals in retirement.

• All withdrawals of Roth savings are free from federal income tax in retirement if the participant is at least 59½ years old and the account has been open for at least five years.

Who can benefit from Roth contributions?

• Younger participants, who are often in lower tax brackets, may benefit from paying taxes now rather than several years later when their income may be taxed at a higher rate.

• Higher-income employees may opt for Roth contributions because they can afford to pay the current taxes now in exchange for the ability to save more in their 401(k) plan on an after-tax basis.

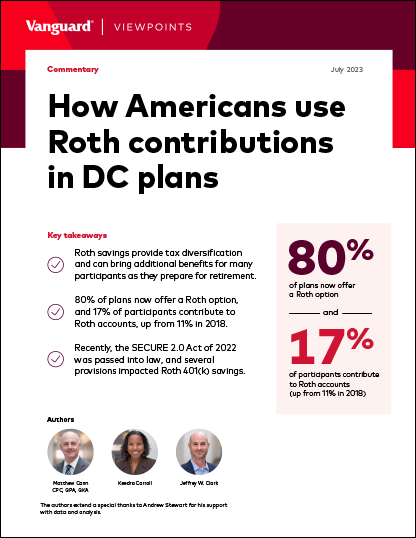

Taking advantage of the Roth option

SECURE 2.0 impact on Roth 401(k) savings

Several provisions in the SECURE 2.0 Act apply to the Roth option:

• Catch-up contributions—Beginning in 2024, participants who have met specific income, age, and deferral limit criteria and wish to make catch-up contributions will be required to make them on a Roth basis.

• Employer contributions—Beginning immediately, retirement plans may offer a Roth option for an employer match or nonelective contribution, as long as those contributions are fully vested.

• Required minimum distributions (RMDs)—Beginning in 2024, participants with Roth accounts are no longer subject to pre-death RMDs.

Next steps for plan sponsors

Plan sponsors should consider adding a Roth option to help participants save up to the maximum regulatory limits with the added benefit of tax diversification. For plans that currently offer a Roth, it’s important to educate participants about the benefits of Roth contributions. Plan sponsors can reinforce the message of the benefit of Roth accounts through:

• Targeted emails.

• Webinars.

• Informational articles.

You can contact your Vanguard representative for more details on Roth adoption, use, and the new SECURE 2.0 provisions.

Notes

- All investing is subject to risk, including the possible loss of the money you invest

- Withdrawals from a Roth IRA or a Roth 401(k) are tax free if you are over age 59½ and have held the account for at least five years; withdrawals taken prior to age 59½ or five years may be subject to ordinary income tax or a 10% federal penalty tax, or both. (A separate five-year period applies for each conversion and begins on the first day of the year in which the conversion contribution is made).

- We recommend that you consult a tax or financial advisor about your individual situation.