While domestic politics can certainly influence asset prices, it is just one of many variables, and our research has shown it to be an inaccurate indicator of future returns. We caution investors against making changes to their portfolios based on political developments.

Vanguard has conducted extensive research on asset returns under various combinations of political power structures, including the party occupying the White House and the composition of Congress, and found no statistically significant relationship. Of course, investor emotions in response to the ongoing news coverage, changes in fiscal policy, and countless other factors can play a role in asset prices over the short term. However, it is challenging to capitalize on these changes, and we believe a long-term perspective is key to investment success.

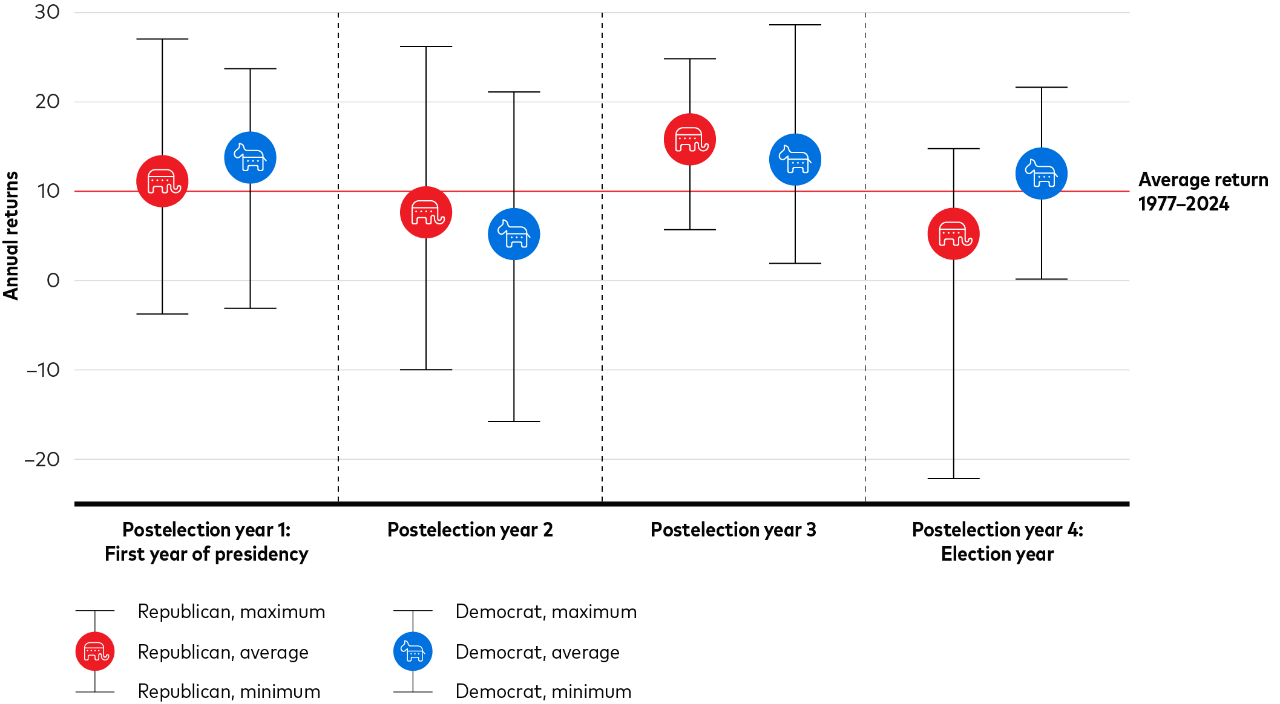

U.S. markets have historically risen over the long term regardless of which political party is in office. As shown below, yearly returns for a 60% equity/40% bond portfolio have generally been positive across all stages of an election cycle under both Democratic and Republican presidencies.

Annual returns for a balanced portfolio regardless of political party

Source: Vanguard calculations using data from Morningstar, Inc.

Note: Data covers period from January 1977 through December 2024. The chart illustrates the average, minimum, and maximum calendar-year return during each of the four years that either political party occupied the White House. The portfolio is 60% stocks and 40% bonds and rebalanced monthly. Returns for the U.S. stock allocation are represented by the S&P 500 Index. Returns for the U.S. bond allocation are represented by the Bloomberg U.S. Aggregate Bond Index. Past performance is no guarantee of future returns. The performance of an index is not an exact representation of any particular investment, as you cannot invest directly in an index.

Source: Vanguard calculations using data from Morningstar, Inc.

Note: Data covers period from January 1977 through December 2024. The initial allocation for the portfolio is 60% U.S. stocks and 40% U.S. bonds. The rebalanced portfolio is returned to a 60% stock/40% fixed income allocation at month-end. Returns for the U.S. stock allocation are represented by the S&P 500 Index. Returns for the U.S. bond allocation are represented by the Bloomberg U.S. Aggregate Bond Index. Past performance is no guarantee of future returns. The performance of an index is not an exact representation of any particular investment, as you cannot invest directly in an index.

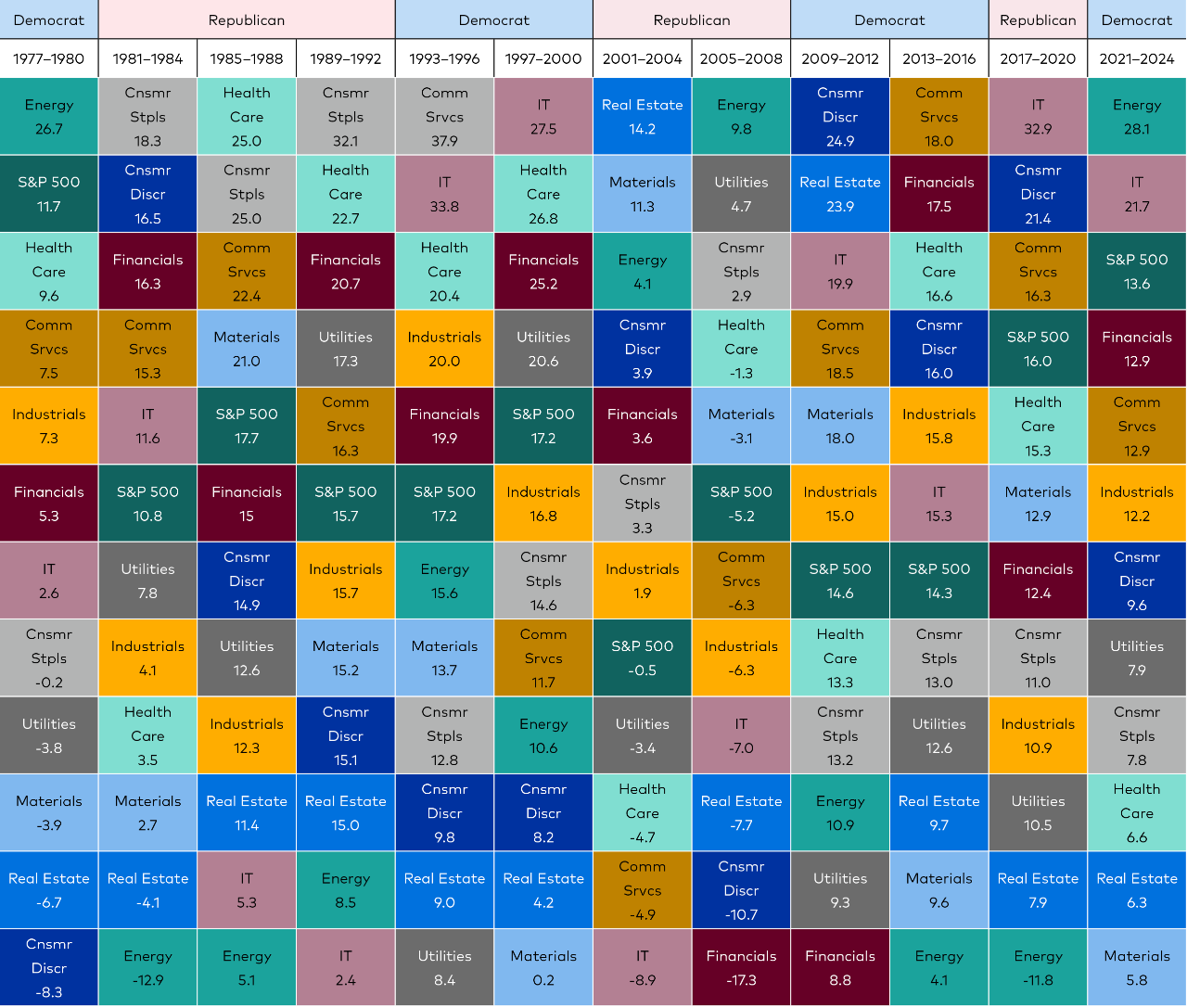

Relative performance of S&P 500 sectors is difficult to predict

Source: Vanguard calculations using data from Morningstar, Inc.

Note: Data covers period from January 1977 through December 2024 for the S&P 500 Index. Sector performance for each period is calculated as an average annualized 4-year total return. Past performance is no guarantee of future returns. The performance of an index is not an exact representation of any particular investment, as you cannot invest directly in an index.

Market volatility can also be an area of concern for investors leading up to and following presidential elections, perhaps a reflection of uncertainty related to policy changes. Again, specific policies can have direct implications for the markets, economy, and investor portfolios. However, making changes to one’s portfolio allocation based on short-term expectations of market volatility comes with challenges and has the potential to negatively affect a participant’s overall retirement saving goals.

Our analysis of equity market returns since 1976 found no general increase in volatility during an election year, or the year immediately following an election year, when compared with longer-term average values. The average annualized volatility of daily returns for the S&P 500 Price Index since 1976 was 17.4% during election years and 13.5% during postelection years. The average volatility for the full 49-year period ending December 2024 was also 17.4%. There has, of course, been variation in the range of volatility in any given year, but as previously mentioned, these drivers of volatility are often unrelated to political outcomes, and investment decisions should be anchored to long-term fundamentals.

Comparison of equity market volatility during election and post election years

Source: Vanguard calculations using daily returns data from FactSet.

Note: Data covers period from January 1976 through December 2024. Volatility is calculated as the annualized standard deviation of daily price returns for the S&P 500 Index during each election and postelection year from 1976 to the present. Past performance is no guarantee of future returns. The performance of an index is not an exact representation of any particular investment, as you cannot invest directly in an index.

Key takeaway

Presidential elections and policy rhetoric can create a lot of noise and may tempt plan participants to deviate from their long-term retirement plan goals. But market movements are difficult to predict, and fundamental factors play a much larger role than political cycles when it comes to portfolio returns. We recommend that investors saving for retirement stick to their long-term strategic asset allocations and avoid being swayed by news or emotions related to political or policy changes.

For additional commentary regarding presidential elections and investment decisions, you may be interested in reading Presidential Elections Matter—But Not So Much When It Comes to Investments.

Notes:

- All investing is subject to risk, including the possible loss of the money you invest.

- There is no guarantee that any particular asset allocation or mix of funds will meet your investment objectives or provide you with a given level of income.

- Diversification does not ensure a profit or protect against a loss.

- Past performance is no guarantee of future results.