Read time: 11 minutes

In this video, Vanguard's Dina Caggiula and Colton Fisher put a little perspective on how 2022’s financial uncertainty affected 401(k) participants. Overall, participants showed great resilience considering inflation was still up, markets were down, and COVID-19 wasn’t quite in the rearview mirror just yet.

However . . .

While How America Saves 2023 reports that plan participation and saving rates were on the rise in 2022, unfortunately, so was the percentage of participants who took hardship withdraws.

And while the increase was more of a slight uptick than a large jump, it may still be an indicator that personal financial well-being for some may not be where it should be.

Source: How America Saves 2023, Vanguard.

What do we mean by that? Basically, the people taking hardship withdrawals, for whatever reason, may be having difficulty meeting their current expenses while still saving for long-term goals like college, a house, or retirement.

This difficulty in making ends meet can happen in trying times like the recent years we’ve all endured. But we’re here to help make sure that each and every participant can create their own version of financial success.

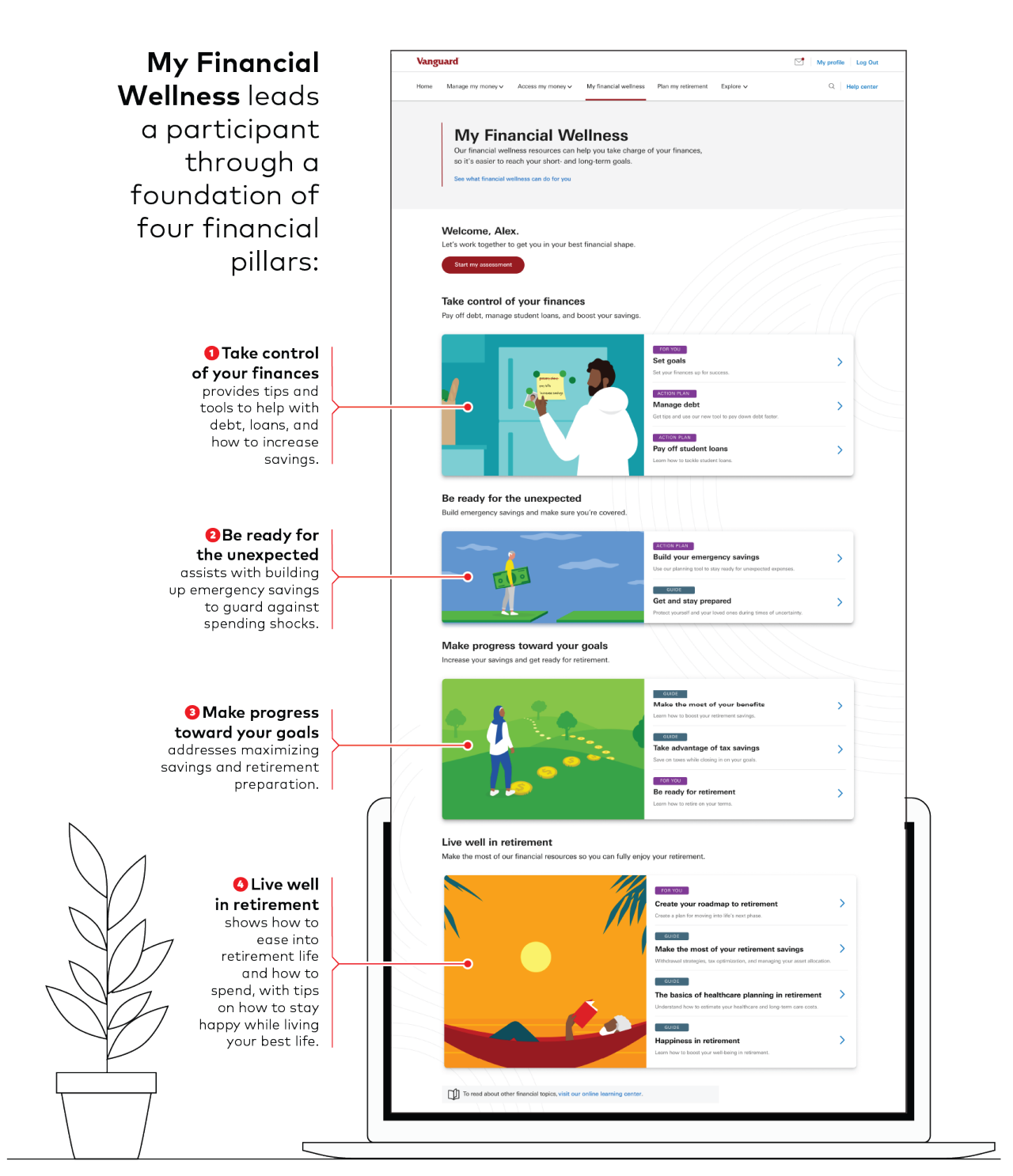

It begins with our personalized participant experience.

This way to financial wellness

Participant engagement with My Financial Wellness and the tools it offers has been stellar. Of those who took the short financial wellness assessment that kicks off a participant’s personalized action plan, 81% completed it.1

And after engaging with the hub itself, users were 50% more likely to take a positive action (like saving more) that could lead to greater retirement success.1

So, help your participants. Give them access to My Financial Wellness, encourage them to interact with it, and help make sure that they’re well on their way to a happier retirement.

For a more comprehensive view of total financial wellness, including steps you can take right now, check out Vanguard’s Guide to Financial Wellness.

A little help from our friends

And thanks to the SECURE 2.0 Act, plan sponsors will soon also be able to help their employees get closer to financial wellness by making matching contributions based on employee student loan payments.

An HSA can help cover current and future medical costs and can bolster financial wellness by offering several tax advantages. Money goes into the account pre-tax*, can grow pre-tax*, and can come out tax-free** if it’s used for qualified medical expenses.

**Distributions must be offset by qualified expenses. See IRS Publication 969 for additional information.

A little (more) help?

But there are times when this can all seem too overwhelming or too stressful for some. They may want someone to give them a hand with their finances—or even someone they can just hand over the keys to and say, “OK, you do it.”

Source: 2023 PwC Employee Financial Wellness Survey.

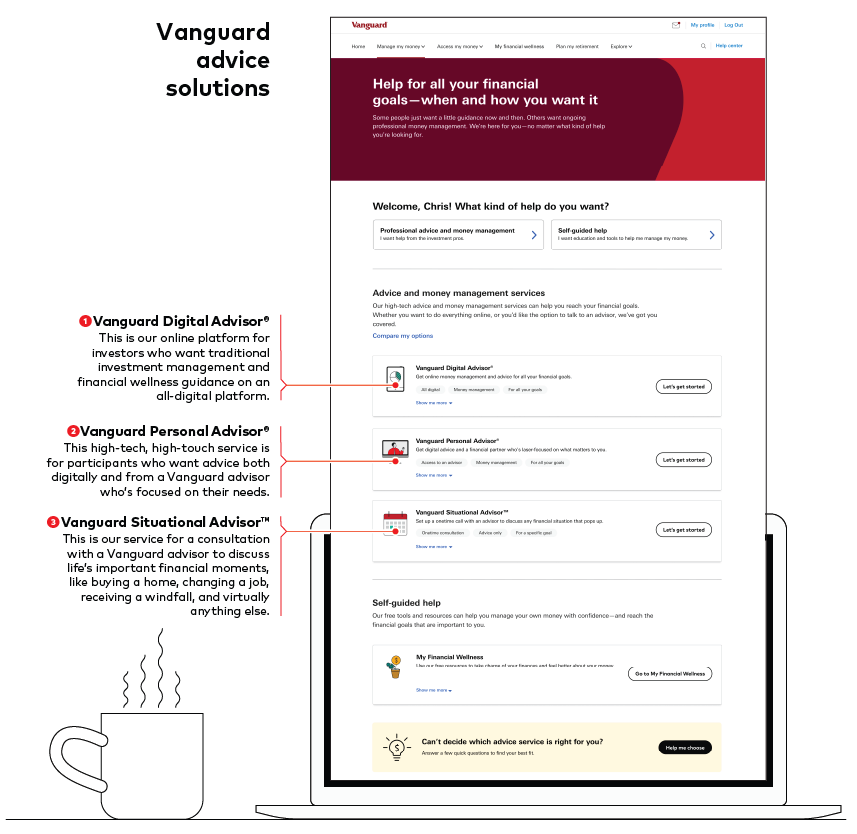

Vanguard advice solutions can help.

We offer a wide array of advice services that can provide as much—or as little—guidance as your participants want. From all-digital solutions to personalized human interaction, our services can offer complete portfolio management and are designed to be totally integrated into the participant wellness experience.

Personalized advice can provide portfolio value, financial value, and even emotional value for your participants.

We customize a portfolio that can meet a participant’s specific needs, help them realize their financial goals, and provide them with greater peace of mind.

In fact, participants with human advisors rated their peace of mind 56% higher than those who invest on their own. Clients with digital advisors rated their peace of mind 12% higher.2

We offer two distinct packages of advice for participants:

- A comprehensive advice suite from Vanguard offering in-the-moment help or ongoing portfolio management for however long a participant would like.

- Third-party advice powered by Edelman Financial Engines offering portfolio management with their independent methodology.

These are two world-class advice services that can keep your participants on the right track for retirement. And thanks to many sponsors, 77% of participants now have access to an advice service, according to How America Saves 2023.

Help your participants with their financial well-being. Consider making advice available in your plan. To learn more, check out our advice page.

Like advice—but different

Right now, according to How America Saves 2023, 66% of participants have their savings in a professionally managed allocation. These allocations could be in managed account advisory service such as Vanguard Digital Advisor®, in a balanced fund, or in, what many see as a counterpart to advice, a target-date fund.

Like a managed account advisory service, a target-date fund will automatically adjust the allocation of a participant’s portfolio over time based on when the participant thinks they’re going to retire—without further involvement from the participant.

Given that, what’s wrong with simply having a target-date fund instead of signing up for an advice service? Well, nothing.

We don’t see advice and target-date funds as an either/or choice. Rather, they complement each other. Target-date funds are very good at moving participants into more age-appropriate portfolios.

Source: Vanguard, 2023.

They can also simplify investing. With a target-date fund, a participant doesn’t have to worry too much about portfolio construction, asset allocation, or rebalancing. Because the target-date fund can take care of that. This is huge for people who don’t want to deal with the technicalities of investing.

However, it’s important to note that while target-date funds can simplify investing, a participant should still monitor their target-date fund to ensure that its portfolio is still in line with their situation and can meet their saving goals and objectives.

Still, as How America Saves 2023 reports, the rise in target-date fund use over the last 10 years indicates 59% of participants are happy to let target-date funds do the work for them.

But there’s a trade-off. A target-date fund isn’t personalized like an advice service. Rather, it invests for a broad range of investors who want to retire in a given year.

On the other hand, our advice is personalized to the individual participant, and may be more capable of addressing more of a participant’s specific financial concerns.

The ultimate choice comes down to one’s personal preference and the complexity of their individual situation.

An extra layer of personalization

Our advice services, target-date funds, and My Financial Wellness are all designed to provide an integrated, personalized wellness experience so that your participants can achieve financial well-being, reach their goals, and stay on the path toward retirement success.

But if you’d like to further explore any element of financial wellness, just reach out to your Vanguard representative. Together, we can help build a brighter and financially solid future for your participants.

Enjoy this article? Read more Vanguard Viewpoints.

Notes:

1. Vanguard, 2023.

2. Quantifying the Investor’s View on the Value of Human and Robo-Advice. Vanguard, 2022.

For more information about Vanguard funds, visit vanguard.com to obtain a prospectus or, if available, a summary prospectus. Investment objectives, risks, charges, expenses, and other important information about a fund are contained in the prospectus; read and consider it carefully before investing.

All investing is subject to risk, including the possible loss of the money you invest. Diversification does not ensure a profit or protect against a loss.

Investments in target-date funds are subject to the risks of their underlying funds. The year in the fund name refers to the approximate year (the target date) when an investor in the fund would retire and leave the workforce. The fund will gradually shift its emphasis from more aggressive investments to more conservative ones based on its target date. An investment in the target-date fund is not guaranteed at any time, including on or after the target date.

Student loan debt services are provided by Candidly. Candidly is not affiliated with The Vanguard Group, Inc., Vanguard Marketing Corporation, or any of their affiliates. The student loan debt services do not provide investment advice or recommendations, but rather student loan debt management guidance and education.

Vanguard Digital Advisor and Vanguard Personal Advisor are provided by Vanguard Advisers, Inc., a federally registered investment advisor. Go to https://personal.vanguard.com/pdf/vanguard-digital-advice-brochure.pdf for important details about these services. Vanguard Digital Advisor’s and Vanguard Personal Advisor’s financial planning tools provide projections and goal achievement forecasts that are hypothetical in nature. They are provided for educational purposes only and are not guarantees of future results.

Vanguard Personal Advisor is provided by Vanguard Advisers, Inc. (VAI), a registered investment advisor. Please review the Vanguard Personal Advisor brochure for important details about this service. Vanguard Personal Advisor’s financial planning tools provide projections and goal forecasts, which are hypothetical in nature, do not reflect actual investment results, and are not guarantees of future results.

Vanguard Situational Advisor is provided by Vanguard Advisers, Inc. (VAI), a registered investment advisor. Eligibility restrictions may apply.

Neither VAI nor Vanguard Situational Advisor can guarantee a profit or prevent a loss.

The Vanguard Group has partnered with Financial Engines Advisors L.L.C. (FEA) to provide subadvisory services to the Vanguard Managed Account Program and Personal Online Advisor. FEA is an independent, federally registered investment advisor that does not sell investments or receive commission for the investments it recommends with respect to the services which it is engaged in as subadvisor for Vanguard Advisers, Inc. (VAI). Advice is provided by Vanguard Advisers, Inc. (VAI), a federally registered investment advisor and an affiliate of The Vanguard Group, Inc. (Vanguard). Vanguard is owned by the Vanguard funds, which are distributed by Vanguard Marketing Corporation, a registered broker-dealer affiliated with VAI and Vanguard. Neither Vanguard, FEA, nor their respective affiliates guarantee future results. Vanguard will use your information in accordance with Vanguard’s Privacy Policy.

Edelman Financial Engines® is a registered trademark of Edelman Financial Engines, LLC. All rights reserved. Used with permission.