Pounding the pavement for plan sponsors

Who: Plan sponsors

What: Plans between $5M and $50M in assets

Why: Plan sponsors are looking for support with:

- Annual investment reviews.

- Rollover services.

- Investment committee meetings.

- Participant guidance.

- Participant advice.

- Fiduciary duties.

3(21) services

As the plan’s investment fiduciary, you’ll provide investment recommendations to the plan sponsor, who may accept or reject them. You’ll also execute the investment decisions for the plan. Ultimately, the plan sponsor retains decision-making authority for the investments and must monitor the performance of the 3(21) fiduciary.

3(38) services

As the plan’s investment manager, you’ll take responsibility for handling the investment lineup. You’ll also have the authority to make necessary changes by selecting, monitoring, removing, and replacing investment options. The plan sponsor is still responsible for monitoring the performance of the 3(38) fiduciary, subject to the terms of the plan document and its investment policy statement.

Coaching participants toward a successful retirement

Who: Participants

What: Retirement plan and financial education and resources

Why: Participants are looking for advisor guidance with:

- Investment selections.

- Saving for retirement.

- Navigating Social Security.

- Retirement income planning.

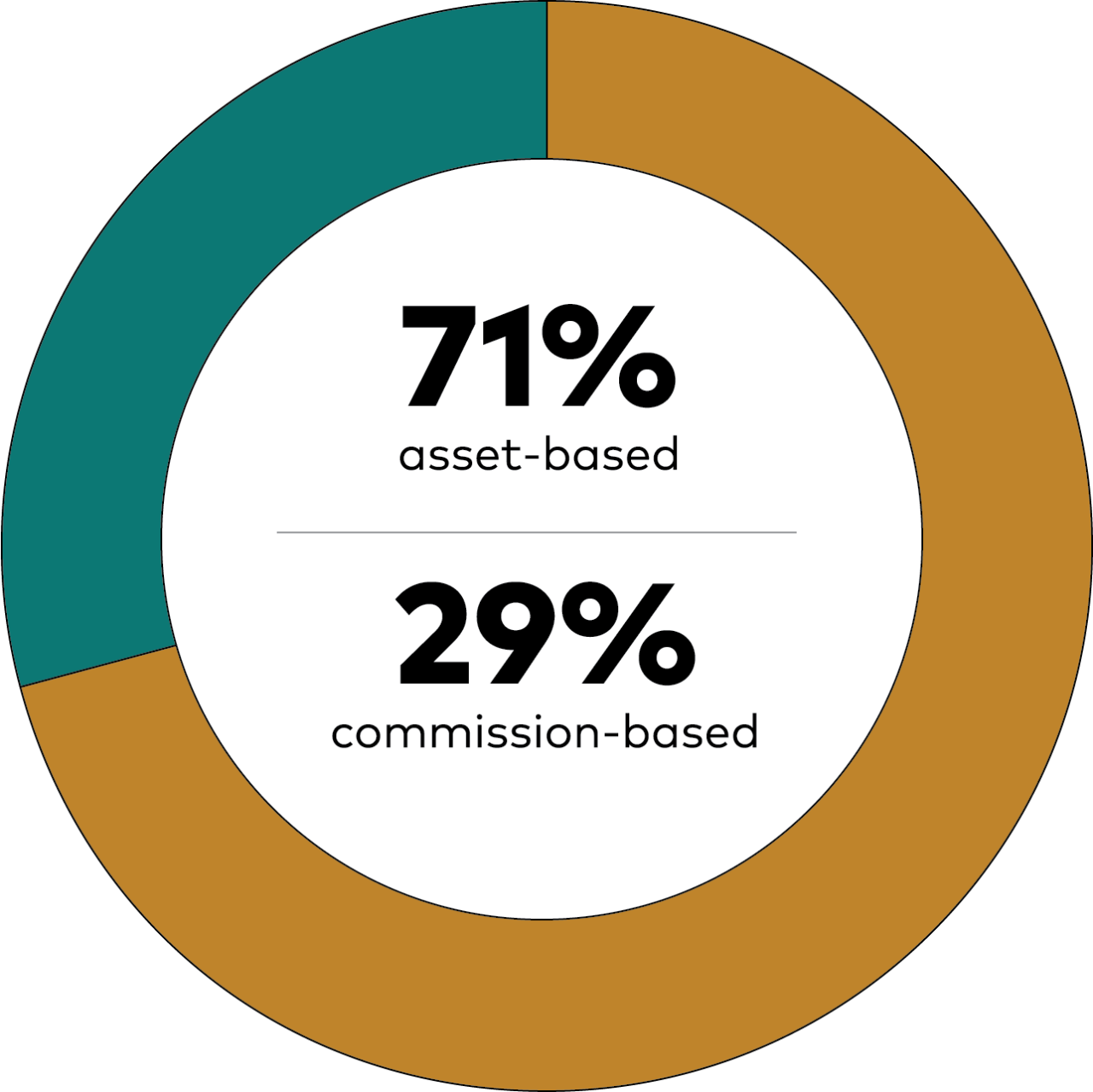

Achieving your personal best with the right fees

Demonstrating your value for the long run

2 The Cerulli Report, U.S. Retirement End-Investor 2023.

3 Capital One CreditWise Survey, 2023.