How America Saves contains data that spans the entire retirement ecosystem, from how plan sponsors are evolving their retirement plans to how participants are interacting with their accounts. Many plan sponsors use the data to benchmark the health of their existing plan and participants. The report not only is a renowned tool in the DC space but also acts as a key input for the Vanguard Life-Cycle Investing Model (VLCM), which we use to validate the design of Vanguard Target Retirement Funds. Specifically, we use How America Saves to evaluate current assumptions regarding investor behavior and look for trends that may drive changes to those assumptions down the line.

As in previous editions, How America Saves 2024 contains several data points that allow plan sponsors and consultants to measure their plans against median statistics for categories such as withdrawal rates, loans outstanding, and average equity allocation. Plan sponsors can also compare their benefits packages against plans with similar asset and participant base sizes and evaluate how their retirement compensation, particularly matching and vesting schedules, compares with that within the broader DC space.

This article highlights some key trends from the 2024 report, specifically those that relate to participants who are invested in TDFs. It also sheds light on how changes in regulation, such as the passing of the SECURE 2.0 Act, may impact TDF investing and spending patterns.

Insights to make informed decisions

How America Saves is prepared by Vanguard’s Strategic Retirement Consulting (SRC) group, which is currently under the direction of Senior Research Analyst Jeff Clark. Drawing upon its expertise, data, and thought leadership, the SRC group focuses on driving differentiated outcomes for plan sponsors and their participants.

Clark and his team spend countless hours reviewing the participant data gathered from systems dedicated to Vanguard’s recordkeeping business to identify trends and develop useful insights that benefit both our plan sponsor clients and goals-based investment options, like TDFs. As a qualified default investment alternative (QDIA), TDFs have simplified the asset allocation process and have shown the ability to meaningfully improve retirement outcomes for millions of participants.

Increased availability of TDFs has improved retirement saving outcomes

“The adoption of TDFs by 96% of plan sponsors is a testament to their significance within the defined contribution space,” Clark says. “While adoption statistics at the plan level speak to the impact of TDFs, the shift in average equity weights by age demographic is amazing. If you look at the data going back to 2005, it shows a monumental shift. More importantly, the data as of year-end 2023 shows that the equity weight now almost mirrors the Vanguard TDF glide path.”

Research findings from How America Saves 2024 show that as TDF use increases, portfolio trading decreases. Another interesting takeaway from the report, Clark says, is related to participants staying the course. Participants with professionally managed portfolios—specifically those that include TDFs and managed account advisory services—are less likely to see extreme equity allocations and variability in returns.1

"With all-in-one options like TDFs becoming more prominent, investors not only benefit from the age-appropriate allocations and continuous rebalancing during volatile markets but are also far less likely to trade when compared with all other investors,” Clark explains. “This is backed by the fact that 2023 was the lowest year ever for participant exchanges—demonstrating a willingness to stay the course despite uncertainty in the market.”

A look ahead at TDF investing

As the largest provider of TDFs in the world, and one of the largest providers of DC administration services in the country, Vanguard is uniquely positioned to address the complexities that result from the ongoing evolution of retirement programs.2 Just as we took a proactive approach at the onset of target-date adoption within QDIAs, we continue to monitor the impact that regulatory changes have on participants’ abilities to reach their financial goals. According to Clark, one influential piece of legislation that has made an impact on the DC space is the SECURE 2.0 Act, which passed as a part of the 2023 omnibus spending bill and focused on encouraging U.S. investors, specifically those within company-sponsored plans, to save for retirement.

“One notable provision from SECURE 2.0 was increasing the required minimum distribution age from 72 up to 75 in 2033,” Clark says. “Vanguard Target Retirement Funds currently complete derisking at age 72 in alignment with our data that shows that is the actual age that people start pulling money from their retirement accounts. While Vanguard’s position is tied to investment behavior and not the explicit required minimum distribution age, it will be interesting to see whether this regulation alters participant behavior materially.”

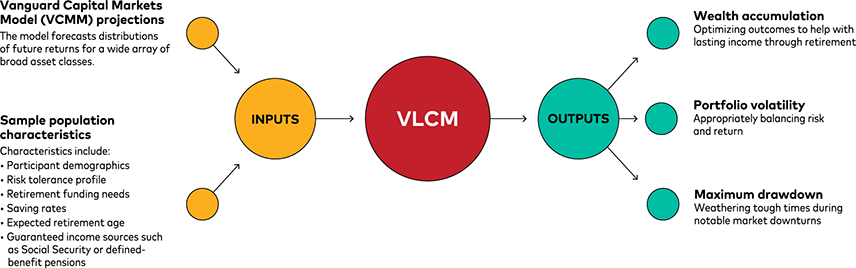

As previously mentioned, Clark and his team have a wealth of knowledge in the DC space that guides our approach to TDFs. We use data leveraged from How America Saves for analysis related to our Target Retirement Funds, including our annual glide-path revalidation process. As shown in Figure 2, that process starts with participant population behavior and characteristic assumptions.

The insights gleaned from investor behavior give us the tools needed to enhance the VLCM, which provides a rigorous framework for evaluating our glide-path decisions and ensuring that they remain appropriate for participants. Made up of multiple inputs, our framework focuses on investor retirement outcomes and aims to strike a balance between two primary objectives of investment portfolios: growth to provide wealth to meet retirement spending needs and stability to provide comfort in volatile markets, particularly for those near or in retirement.

* Select population characteristics and outputs were used in this example and not meant to be exhaustive of all inputs and outputs included in the VLCM analysis.

Source: Vanguard.

Our commitment to research and improving retirement saving

1 Highlighting the value of managed portfolios. Vanguard, September 2023.

2 DC assets are based on AUM in both Vanguard-administered plans and those administered by others. Other figures are based on AUM market share of the TDF industry. Sources: Vanguard and Morningstar, Inc., as of December 31, 2023.

Notes:

- For more information about Vanguard funds, visit vanguard.com to obtain a prospectus or, if available, a summary prospectus. Investment objectives, risks, charges, expenses, and other important information are contained in the prospectus; read and consider it carefully before investing.

- Investments in Target Retirement Funds are subject to the risks of their underlying funds. The year in the fund name refers to the approximate year (the target date) when an investor in the fund would retire and leave the workforce. The fund will gradually shift its emphasis from more aggressive investments to more conservative ones based on its target date. An investment in a Target Retirement Fund is not guaranteed at any time, including on or after the target date.

- All investing is subject to risk, including the possible loss of the money you invest. There is no guarantee that any particular asset allocation or mix of funds will meet your investment objectives or provide you with a given level of income. Diversification does not ensure a profit or protect against a loss.

- The Vanguard Life-Cycle Investing Model (VLCM) is designed to identify the product design that represents the best investment solution for a theoretical, representative investor who uses the target-date funds to accumulate wealth for retirement. The VLCM generates an optimal custom glide path for a participant population by assessing the trade-offs between the expected (median) wealth accumulation and the uncertainty about that wealth outcome, for thousands of potential glide paths. The VLCM does this by combining two sets of inputs: the asset class return projections from the VCMM and the average characteristics of the participant population. Along with the optimal custom glide path, the VLCM generates a wide range of portfolio metrics such as a distribution of potential wealth accumulation outcomes, risk and return distributions for the asset allocation, and probability of ruin, such as the odds of participants depleting their wealth by age 95.

- The VLCM inherits the distributional forecasting framework of the VCMM and applies to it the calculation of wealth outcomes from any given portfolio.

- The most impactful drivers of glide-path changes within the VLCM tend to be risk aversion, the presence of a defined benefit plan, retirement age, saving rate, and starting compensation. The VLCM chooses among glide paths by scoring them according to the utility function described and choosing the one with the highest score. The VLCM does not optimize the levels of spending and contribution rates. Rather, the VLCM optimizes the glide path for a given customizable level of spending, growth rate of contributions, and other plan sponsor characteristics.

- A full dynamic stochastic life-cycle model, including optimization of a savings strategy and dynamic spending in retirement is beyond the scope of this framework.