To provide small-business plan sponsors and advisors with valuable benchmarking data, Vanguard will release How America Saves 2025: Small Business Edition this fall. This report, a supplement to our How America Saves 2025 research, may also help retirement-wealth advisors gain insights into small-business retirement plans.

What follows is a preview of the supplement. It’s an examination of retirement plan data from Vanguard Retirement Plan Access™ (VRPA), which is Vanguard’s comprehensive service for small-business retirement plans. Through VRPA, we were serving about 21,200 plan sponsors and approximately 1 million participants as of year-end 2024.

2024 in perspective

There were several notable economic trends in 2024. The U.S. economy remained strong with real gross domestic product growth. Inflation eased toward the Federal Reserve's target, while unemployment stayed low and real earnings rose. Strong consumer spending followed.

However, while the Federal Reserve began to lower the federal funds rate during the second half of the year, mortgage rates remained elevated, and household debt continued to rise. Meanwhile, the S&P 500 ended with a robust gain of 25%, while the U.S. bond market saw a modest gain of 1%.

Despite all that, our initial findings reveal that participant retirement plan behaviors, in both small and large plans, remained largely unaffected in 2024.

Small business retirement plan insights

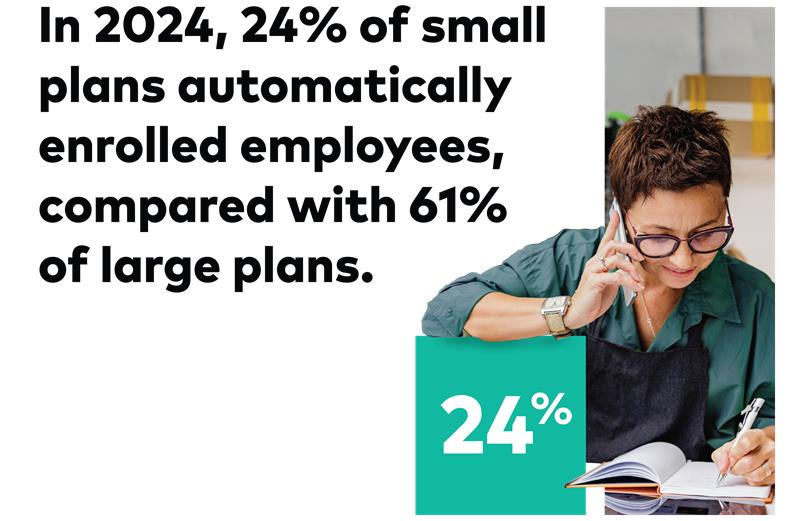

Plan design differences

Small plans and large plans employ different plan designs, and some differences are significant. The most important difference is with the use of automatic enrollment.

In 2024, 24% of small plans automatically enrolled employees, compared with 61% of large plans. Three in 4 large plans offered immediate eligibility; 1 in 4 small plans did.

Participation rates

Deferral rates

Account balances

Exchange activity

Participant trading, or exchange activity, is the movement of existing account assets from one plan investment option to another. Excluding those in a managed account program, only 5% of small-plan participants initiated an exchange in 2024, a rate in line with large plans.

Pure TDF investors, those who hold a single TDF, not only benefit from age-appropriate equity allocations and continuous rebalancing but are also far less likely to trade than other investors.

Loan and withdrawal use

Before retirement, there are generally two ways plan participants can access their retirement savings: loans or in-service withdrawals.

Loans are widely offered by DC plans. In 2024, 7 in 10 small plans permitted loans, compared with 8 in 10 large plans. Only 6% of small-plan participants who were offered a loan also had a loan outstanding at year-end 2024, compared with 13% of large-plan participants.

Overall, hardship withdrawal activity has increased over the past few years. In 2024, 2.0% of small-plan participants initiated a hardship withdrawal, up slightly from 1.7% in 2023. Large-plan participants were about 2.5 times more likely to take a hardship withdrawal than participants in small plans. One likely reason for this difference is automatic enrollment, which helps more workers save for retirement, especially lower-income workers. Large plans, likely to include more lower-income participants, tend to have higher withdrawal rates. And for a small subset of workers facing financial stress, hardship withdrawals may serve as a safety net that otherwise may not have been available without plan-implemented automatic solutions.

The hardship withdrawal data from both small and large plans points to the importance of financial wellness and establishing an emergency savings account to help cover unexpected expenses.

Conclusion

Smart plan design features—automatic enrollment with automatic increases, higher employee default rates, and competitive employer contributions—can remove barriers to saving for retirement and help workers improve their retirement readiness.

Additionally, employees have many competing financial priorities, and retirement savings is just one of them. Student loans, health care savings, credit card debt, and emergency savings goals, to name just a few, can be daunting and complex for many workers. Plan sponsors can help support their employees with a cost-efficient, high-quality advice offer as well as guidance on financial well-being—two valuable services that meet participants wherever they are on their financial journey and help provide personalized solutions for their goals.

This is just a glimpse of the insights we will share in How America Saves 2025: Small Business Edition. We hope this preview can help small-business plan sponsors and advisors better prepare participants for retirement. Look for the full report this fall.

Source:

1 U.S. Small Business Administration, 2024.

Notes:

- All investing is subject to risk, including the possible loss of the money you invest. Diversification does not ensure a profit or protect against a loss.

- Past performance is not a guarantee of future return.

- Investments in target-date funds are subject to the risks of their underlying funds. The year in the fund name refers to the approximate year (the target date) when an investor in the fund would retire and leave the workforce. The fund will gradually shift its emphasis from more aggressive investments to more conservative ones based on its target date. An investment in target-date funds is not guaranteed at any time, including on or after the target date.

- Unless otherwise indicated, all data sourced from Vanguard, 2025.